You already know this uncomfortable truth: most portfolios do not fail because of bad asset selection. They fail because of bad assumptions. In 2008, diversified portfolios collapsed together. In 2020, risk models built on decades of data broke in weeks. In 2022–2023, the fastest interest-rate tightening in forty years punished both equities and bonds at the same time. Each episode shared a pattern. Wealth managers relied on forecasts. Markets punished them for it.

This is why financial scenario planning has moved from a back-office exercise to a front-line discipline in modern wealth management. The firms that protected capital did not predict the future. They rehearsed multiple futures and prepared clients for each one.

If your advisor still presents a single “base case” projection, you should ask why. Markets never deliver one outcome. Why should your plan assume only one?

Why Scenario Planning Replaced Forecasting in Wealth Management

Forecasts flatter certainty. Scenario planning challenges it.

Traditional forecasting answers a narrow question: what is most likely to happen next? Scenario planning asks a harder one: what happens to your wealth if the least comfortable outcomes occur?

Wealth managers began adopting scenario planning seriously after three structural shifts:

- Macro volatility compressed timeframes. Economic cycles now move faster than planning cycles.

- Correlation regimes changed. Assets once considered diversifiers now move together under stress.

- Client risk tolerance exposed itself as fragile. Many investors overestimated their ability to hold through drawdowns.

The data backs this up. Morningstar analysis of investor behavior shows that poor timing and panic-driven exits reduce realized returns by 1–2 percentage points annually for many retail investors. That gap does not come from asset choice. It comes from surprise.

Scenario planning exists to remove surprise.

What Financial Scenario Planning Really Means in Practice

This is not about Monte Carlo charts that clients ignore. Real financial scenario planning links markets, policy, behavior, and portfolio mechanics.

A professional wealth manager structures scenario planning around four pillars:

- Macro catalysts

Inflation shocks, rate regime shifts, geopolitical escalation, fiscal stress, demographic change. - Market transmission paths

How those catalysts move yields, currencies, credit spreads, and equity valuations. - Portfolio response

What breaks, what hedges work, what correlations fail. - Client decision risk

Where panic, overconfidence, or liquidity needs force suboptimal actions.

If any of these pillars sit outside your planning process, your portfolio remains exposed.

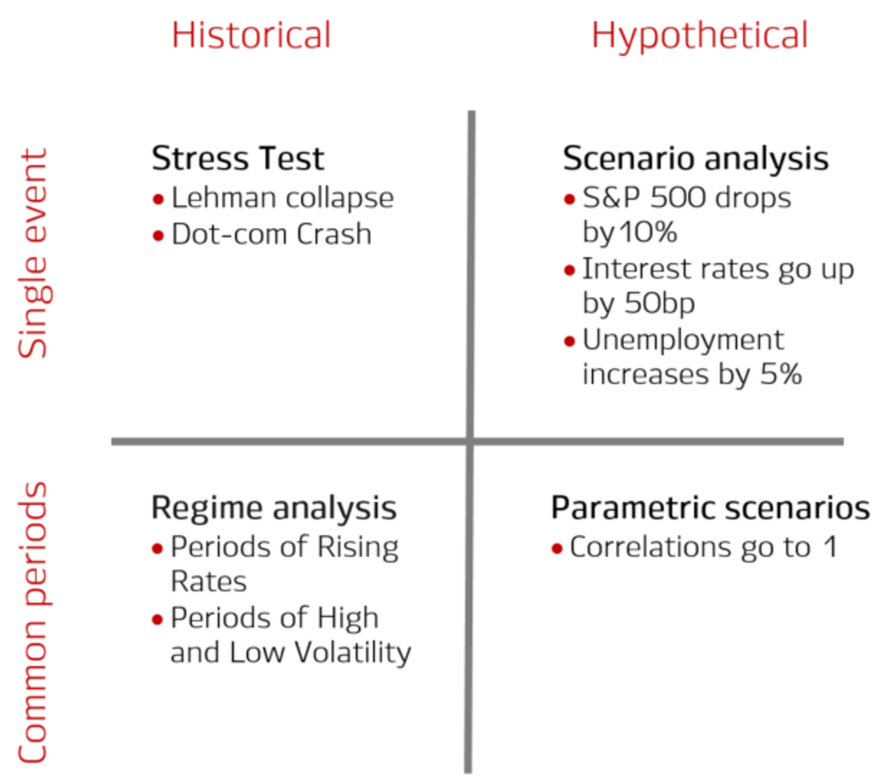

The Core Scenarios Wealth Managers Actually Model

Serious wealth managers do not model dozens of outcomes. They focus on a small set of structurally different worlds.

1. Prolonged High Inflation Without Recession

This scenario haunted portfolios after 2021.

Key assumptions:

- Policy rates stay elevated for years

- Wage growth remains sticky

- Real returns compress

Portfolio stress points:

- Long-duration bonds underperform

- Growth equities reprice downward

- Cash regains relevance

Managers test:

- Real asset exposure

- Floating-rate instruments

- Pricing power in equity holdings

2. Hard Landing Recession

This scenario matters because it forces timing risk.

Key assumptions:

- Credit tightens abruptly

- Earnings fall faster than expected

- Policy support lags markets

Portfolio stress points:

- High-yield credit defaults

- Cyclical equities collapse

- Liquidity dries up

Managers test:

- Downside protection costs

- Cash runway for withdrawals

- Client tolerance for drawdowns

3. Financial System Stress Event

Think 2008 or regional bank failures.

Key assumptions:

- Counterparty risk spikes

- Correlations converge

- Policy response becomes unpredictable

Portfolio stress points:

- Alternatives freeze

- Leveraged strategies unwind

- Safe-haven assets reprice violently

Managers test:

- Liquidity mismatches

- Custodial risk

- Hedging reliability

4. Low Growth, High Debt Stagnation

This scenario receives less attention and causes more damage over time.

Key assumptions:

- Aging demographics

- Persistent fiscal deficits

- Low real returns

Portfolio stress points:

- Traditional 60/40 stagnates

- Income strategies underdeliver

- Inflation-adjusted goals slip

Managers test:

- Return expectations

- Spending assumptions

- Tax efficiency

These scenarios are not predictions. They are stress lenses.

How Wealth Managers Translate Scenarios Into Portfolio Design

Scenario planning fails if it stays theoretical. The discipline matters only when it changes how portfolios are built.

Asset Allocation Under Scenario Constraints

Instead of optimizing for return, managers optimize for survivability.

That changes allocation decisions:

- Lower concentration risk across asset classes

- Reduced reliance on historical correlations

- Explicit liquidity tiers inside portfolios

Many firms now classify assets by liquidity under stress, not just by asset class. That shift came directly from scenario analysis after 2020.

Risk Budgeting Replaces Static Models

Value at Risk models assume normal markets. Scenario planning assumes markets break.

Wealth managers assign risk budgets based on:

- Maximum tolerable drawdown

- Behavioral breaking points

- Cash flow obligations

If a scenario breaches those limits, the portfolio changes. This process removes emotion from decisions before emotion appears.

Behavioral Risk Is the Most Underestimated Scenario

Markets do not destroy wealth alone. Investors finish the job.

During March 2020, equity markets fell roughly 34 percent in weeks. Fund flow data shows massive retail outflows near the bottom. Many investors never re-entered.

Scenario planning now includes decision simulations:

- Would you sell after a 20 percent drawdown?

- Would you demand income when dividends fall?

- Would you tolerate illiquidity under stress?

Wealth managers who ask these questions early protect clients from themselves.

If your plan assumes perfect discipline, it is already broken.

How Institutional Practices Influenced Private Wealth Scenario Planning

Scenario planning matured inside institutions long before private wealth adopted it.

Pension funds, sovereign wealth funds, and insurers stress-tested portfolios against tail risks for decades. After the global financial crisis, regulators forced banks to formalize this discipline.

The US Federal Reserve institutionalized stress testing through CCAR programs after 2009. European regulators followed similar paths. While private wealth does not face regulatory stress tests, the methodology migrated downstream.

Firms that serve ultra-high-net-worth clients adopted institutional tools first. Mass affluent platforms followed later.

This trickle-down explains the quality gap between advisors today.

Scenario Planning and Interest Rate Regime Shifts

Interest rates shaped portfolio outcomes more than any variable between 2022 and 2024.

For forty years, falling rates bailed out bad decisions. That assumption no longer holds.

Wealth managers now model:

- Rate volatility instead of direction

- Yield curve inversion persistence

- Policy error risk

Scenario analysis revealed an uncomfortable truth. Bond duration once acted as insurance. In rising rate regimes, it becomes a liability.

That insight changed how advisors structure fixed income today.

Liquidity Planning as a Scenario Discipline

Liquidity kills more portfolios than volatility.

During stress events:

- Private funds gate redemptions

- Real estate transactions freeze

- Credit markets widen spreads

Scenario planning forces wealth managers to map liquidity needs against liquidity supply.

This includes:

- Emergency spending needs

- Tax obligations under asset sales

- Capital calls from private investments

If your portfolio cannot meet obligations in a stress scenario, returns do not matter.

Scenario Planning for Tax and Regulatory Shifts

Markets are not the only risk.

Wealth managers increasingly model:

- Capital gains tax increases

- Estate tax threshold changes

- Cross-border regulation shifts

These scenarios affect after-tax returns more than market noise for high-net-worth families.

A portfolio that performs well before tax may fail its real objective after tax. Scenario planning exposes this gap early.

Technology Changed the Scale, Not the Judgment

Modern planning software runs thousands of simulations instantly. That speed creates false confidence.

Tools do not replace judgment. They amplify it.

The best wealth managers use technology to:

- Visualize drawdowns

- Compare scenario impacts

- Communicate risk clearly

They avoid outsourcing thinking to algorithms.

If your advisor cannot explain scenario outcomes without charts, you should question the process.

How Scenario Planning Shapes Client Conversations

Scenario planning changes the relationship between advisor and client.

Conversations shift from:

- “What return can I expect?”

to - “What can go wrong and how do we respond?”

This reframing builds trust because it respects your intelligence. It treats you as a decision-maker, not a passenger.

Clients who understand scenarios:

- Panic less

- Stay invested longer

- Make fewer reactive changes

Those outcomes compound.

Real-World Example: Two Portfolios, One Crisis

During the 2022 rate shock, many balanced portfolios lost over 15 percent. Some lost far more.

Wealth managers who had run inflation and rate-hike scenarios reduced duration earlier. They raised cash intentionally. They diversified income sources.

The difference was not genius. It was preparation.

Scenario planning does not eliminate losses. It controls damage.

When Scenario Planning Fails

This discipline fails under three conditions:

- Scenarios become marketing tools instead of decision tools

- Advisors ignore uncomfortable outputs

- Clients refuse to accept trade-offs

Every scenario reveals opportunity cost. Protection costs money. Liquidity reduces upside. Discipline limits speculation.

If you want unlimited upside with no downside, scenario planning cannot help you. Markets will teach the lesson instead.

The Question You Should Ask Your Wealth Manager

Not “What will happen next?”

Ask this instead:

- What scenarios threaten my plan?

- Which ones hurt the most?

- What actions are pre-approved if they occur?

If those answers do not exist, you are relying on hope.

Hope is not a strategy.

The Strategic Advantage of Financial Scenario Planning

Financial scenario planning does one thing exceptionally well. It aligns portfolios with reality rather than narratives.

Markets do not reward conviction. They reward preparation.

The next crisis will not look like the last. The only constant is uncertainty. Wealth managers who accept that fact build portfolios that survive. Those who ignore it rebuild portfolios after damage occurs.

Your choice lies in which side you stand.

4

References

Federal Reserve Comprehensive Capital Analysis and Review Overview

https://www.federalreserve.gov/supervisionreg/ccar.htm

Morningstar Investor Behavior Research

https://www.morningstar.com/articles/investor-behavior-gap

IMF Global Financial Stability Report

https://www.imf.org/en/Publications/GFSR

OECD Long-Term Investment and Stagnation Studies

https://www.oecd.org/finance/long-term-investment.htm