Markets like to present themselves as rational machines. Prices move because information changes. Investors weigh risk against return. Capital flows to its most efficient use. That story no longer survives contact with reality, if it ever did. Over the past decade, markets have swung violently on rumors, tweets, memes, fear cycles, and viral narratives. You have seen asset prices surge without earnings, collapse without fundamentals, and reverse direction within hours. Traditional finance still struggles to explain this. Behavioral finance does not.

Behavioral finance matters more than ever because markets today reflect human behavior at internet speed. Decisions that once unfolded over weeks now happen in seconds. Retail investors trade alongside institutions with similar tools but very different incentives. Algorithms amplify emotion rather than neutralize it. Central banks inject liquidity while social media injects belief. If you still analyze markets assuming rational actors, you misread risk, misprice opportunity, and underestimate fragility.

This is not a philosophical debate. It affects your portfolio, your retirement, your business decisions, and public policy. Behavioral finance has moved from academic curiosity to operational necessity.

The Market Is No Longer a Classroom Example

In early 2020, global markets erased trillions of dollars in weeks. Fundamentals did not deteriorate at the same pace. In 2021, meme stocks rallied hundreds of percent with no change in cash flows. In 2022, inflation fear triggered synchronized selloffs across asset classes. In 2023 and 2024, artificial intelligence narratives lifted valuations before revenues followed. Each episode shared a common driver: collective behavior.

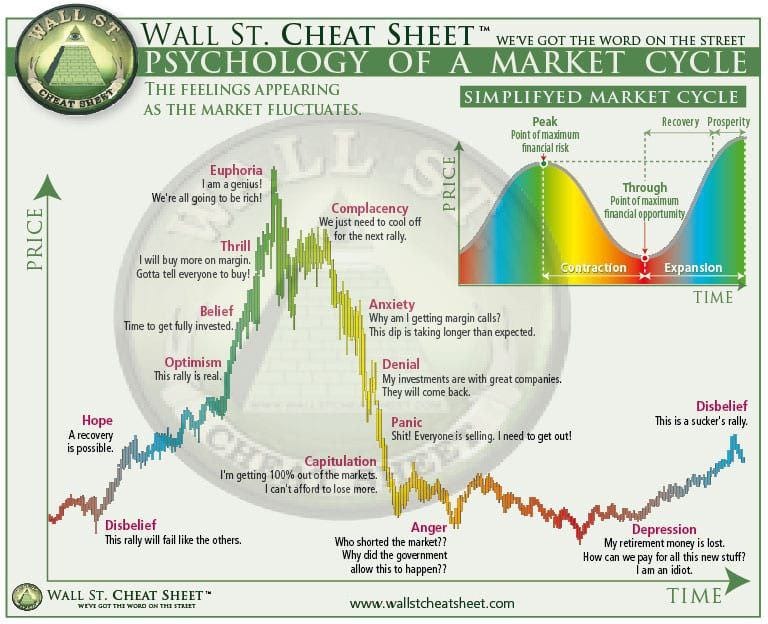

Classical finance models assume that investors update beliefs logically when new information arrives. Real markets show something else. Investors anchor to prior prices, chase trends, panic under uncertainty, and overreact to recent news. Behavioral finance explains why.

The field gained global recognition through the work of Daniel Kahneman and Amos Tversky, whose research demonstrated that humans rely on mental shortcuts under uncertainty. Those shortcuts help in daily life. In markets, they distort judgment.

Today, those distortions scale instantly. A bias expressed by one influential voice can move millions of investors within minutes. That reality forces you to rethink how markets function.

Behavioral Finance Is No Longer About Small Errors

Early critics dismissed behavioral finance as a study of minor deviations from rationality. That argument collapsed once trading platforms, zero-commission access, and social media entered the picture. Behavioral effects no longer stay small. They cascade.

Consider what changed:

- Trading costs dropped to near zero, removing friction that once slowed impulsive decisions

- Mobile apps turned investing into a constant, gamified activity

- Financial news shifted from periodic reporting to continuous commentary

- Social validation through likes, shares, and screenshots reinforced herd behavior

These conditions amplify biases such as overconfidence, loss aversion, and confirmation bias. The result is not random noise. It is patterned behavior that repeats across cycles.

Behavioral finance gives you tools to identify those patterns before they peak.

Loss Aversion Shapes Risk More Than Returns

You feel losses more intensely than gains. That fact drives many poor decisions. Investors hold losing positions too long, hoping to break even. They sell winning positions too early to lock in comfort. This behavior creates predictable market outcomes.

Loss aversion explains:

- Why selloffs accelerate once key price levels break

- Why recoveries often stall near previous highs

- Why volatility spikes during periods of uncertainty

During the 2008 financial crisis, investors did not gradually adjust risk exposure. They rushed to safety once fear crossed a psychological threshold. The same pattern appeared during pandemic-driven crashes and inflation scares.

If you manage money or policy without accounting for loss aversion, you underestimate downside momentum.

Overconfidence Drives Excessive Trading and Mispricing

Most investors believe they are above average. Markets punish that belief. Overconfidence leads to excessive trading, concentration risk, and underestimation of uncertainty.

Data from multiple brokerage studies show that frequent traders underperform passive strategies after costs. This underperformance persists across markets and generations. The cause is not lack of intelligence. It is overconfidence.

Overconfidence also fuels speculative bubbles. Investors extrapolate recent success into the future. They mistake skill for luck. They ignore base rates.

Behavioral finance forces you to ask uncomfortable questions. Are your recent wins evidence of insight or timing? Are you reacting to data or reinforcing your own narrative?

Herd Behavior Is Rational at the Individual Level

Following the crowd looks irrational from the outside. From the inside, it often feels prudent. When uncertainty rises, social cues replace independent analysis. You infer information from others’ actions.

Herd behavior explains why:

- Asset correlations rise during stress

- Valuations detach from fundamentals during momentum phases

- Bubbles persist longer than expected

In modern markets, herding accelerates through online communities and algorithmic trend-following. Once a narrative takes hold, dissent becomes costly. Behavioral finance does not mock this behavior. It explains it.

Understanding herd dynamics helps you distinguish between trend participation and blind conformity.

Narrative Economics Now Moves Capital

Economic data matters. Stories move faster. Investors respond to narratives that simplify complexity and assign meaning to uncertainty. Inflation scares, soft landing optimism, artificial intelligence disruption, and deglobalization fears all function as narratives.

Behavioral finance intersects with narrative economics by recognizing that belief systems influence economic outcomes. If enough investors believe a story, prices adjust to validate it, at least temporarily.

You see this dynamic in thematic investing, sector rotations, and speculative runs. Ignoring narratives leaves you reactive. Understanding them gives you context.

Behavioral Finance and Market Crashes

Crashes do not start with data. They start with shifts in perception. Fear spreads nonlinearly. Selling begets selling. Liquidity disappears when everyone seeks it.

Behavioral finance identifies warning signs before crashes escalate:

- Elevated leverage combined with narrow leadership

- Increased sensitivity to negative news

- Overreliance on recent performance

- Moral certainty in bullish narratives

These signals appeared before the dot-com collapse, the global financial crisis, and several regional market crashes. They appear again and again.

You cannot time every crash. You can avoid believing that this time is different.

The Retail Investor Changed Market Structure

Retail participation surged after 2020. This shift altered liquidity patterns and volatility dynamics. Retail investors trade smaller sizes but act in coordinated waves. Platforms that display trending assets reinforce momentum.

Behavioral finance explains why retail flows often chase price rather than value. It also explains why institutions monitor retail sentiment as a market indicator.

This is not about intelligence. It is about incentives, interfaces, and psychology.

Institutional Investors Are Not Immune

Large funds employ sophisticated models and teams. They still answer to human committees, career risk, and performance benchmarks. Behavioral biases influence allocation decisions, risk management, and timing.

Career risk leads to herding among professionals. Managers prefer being wrong with the crowd over right alone. Behavioral finance exposes this dynamic without moral judgment.

Understanding institutional behavior helps you interpret flows and positioning beyond surface-level data.

Central Banks and Behavioral Feedback Loops

Monetary policy influences expectations as much as rates. Forward guidance works by shaping beliefs. When central banks signal confidence or concern, markets respond before policy changes occur.

Behavioral finance highlights feedback loops between policy communication and market behavior. Overreliance on central bank support can breed complacency. Sudden shifts in tone can trigger overreactions.

You see this pattern in rate hike cycles, quantitative easing, and liquidity interventions.

Behavioral Biases in Corporate Decision-Making

Behavioral finance does not stop at investing. Corporate leaders display the same biases. Overconfidence leads to aggressive acquisitions. Anchoring distorts valuation assumptions. Confirmation bias narrows strategic options.

Poor capital allocation often traces back to behavioral errors rather than analytical failures. Boards and investors increasingly incorporate behavioral insights into governance and oversight.

If you analyze companies without considering leadership psychology, you miss material risk.

Technology Amplifies Bias, Not Neutrality

Algorithms do not remove human bias. They encode it. Models trained on historical behavior replicate past patterns, including irrational ones. High-frequency trading can amplify short-term volatility. Recommendation systems reinforce confirmation bias.

Behavioral finance adapts to this reality. It studies how humans interact with machines and how machines magnify human tendencies.

Understanding this interaction matters if you trade, invest, or regulate markets.

Why Behavioral Finance Improves Risk Management

Traditional risk models rely on historical distributions. Behavioral finance focuses on regime shifts driven by psychology. It prepares you for fat tails and nonlinear outcomes.

Practical applications include:

- Stress testing portfolios under panic scenarios

- Adjusting position sizing during euphoric phases

- Incorporating sentiment indicators into risk dashboards

- Recognizing when diversification breaks down

Risk management fails when it assumes calm conditions. Behavioral finance assumes stress.

Education Failed to Keep Up With Reality

Finance education still emphasizes efficient markets and equilibrium models. These frameworks provide structure. They do not describe lived market experience.

Behavioral finance bridges theory and reality. It explains why smart people make poor decisions under pressure. It teaches humility rather than prediction.

For professionals, this shift matters. Clients judge outcomes, not models.

Regulation and Policy Need Behavioral Insight

Market regulation often assumes rational compliance. Behavioral finance reveals how incentives, framing, and defaults shape behavior. Policies that ignore psychology underperform.

Examples include retirement savings design, disclosure rules, and risk warnings. Behavioral insights improve participation and outcomes without coercion.

Policy makers increasingly rely on behavioral research to design effective interventions.

Why You Cannot Afford to Ignore Behavioral Finance

You operate in a market driven by humans, narratives, and feedback loops. Ignoring behavioral finance leaves you blind to the forces shaping prices.

This field does not promise certainty. It offers realism. It asks you to question assumptions, examine incentives, and recognize patterns.

Behavioral finance matters more than ever because markets move on belief before evidence. If you want to manage risk, allocate capital, or interpret policy effectively, you need to understand how people actually behave.

Rational models describe how markets should work. Behavioral finance explains how they do.

References

Thinking, Fast and Slow

https://www.penguinrandomhouse.com/books/207807/thinking-fast-and-slow-by-daniel-kahneman/

Prospect Theory An Analysis of Decision under Risk

https://www.princeton.edu/~kahneman/docs/Publications/prospect_theory.pdf

Shiller Narrative Economics

https://www.aeaweb.org/articles?id=10.1257/jep.31.2.59

Barber and Odean Trading Is Hazardous to Your Wealth

https://faculty.haas.berkeley.edu/odean/papers/tradinghazardous.pdf

OECD Behavioural Insights and Public Policy

https://www.oecd.org/gov/regulatory-policy/behavioural-insights.htm